Home Building Articles

New Homes vs Foreclosures

August 27, 2009

Apples vs. Oranges

Appraisers need regulatory guidelines that acknowledge today's realities.

Related Articles

Save/Share

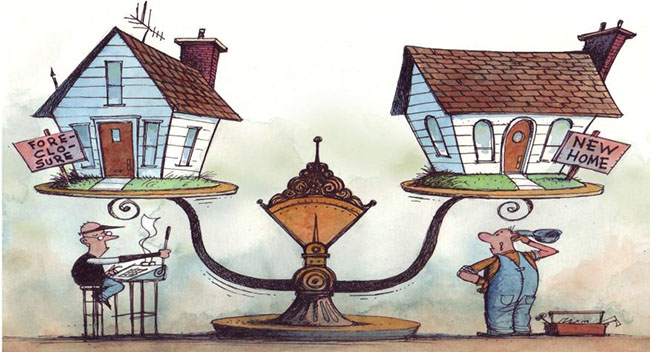

Picture this: For the first time in months a small builder sells a new home. The

sales price cuts the builder's profit to the bone, but it's a reasonable price given

today's housing market. The buyers are well qualified, and everything is going along

smoothly until the appraisal comes in at tens of thousands of dollars less than

the sales price. Why? The local market has been hit hard by the recession and the

comparables include foreclosures and other distressed sales.

Now the builder faces a wrenching dilemma. Does he cut the home's price to be consistent

with the appraisal value and take a loss, or does he cancel the sale even though

it could take a long time to find another buyer and the next appraisal could come

in equally low?

Scenarios like this are playing out daily in markets across the country as the use

of foreclosed and distressed sales as comparables for appraisals on single-family

homes needlessly drives down home values, slows new-home sales, and puts a drag

on the housing recovery.

Equally important, using foreclosed and distressed properties as comparables is

affecting the availability of AD&C credit. Falling appraised values for land and

subdivisions under development have led some financial institutions to stop lending

to developers/builders, to demand additional equity, and even to call performing

loans.

This is a complex situation with many interconnected parts. In the wake of criticism

that lax appraisal standards contributed to the economic and housing crisis, appraisal

standards and procedures were tightened earlier this year. But now the pendulum

has swung too far, and reports of homes failing to appraise at the sales price,

or even construction cost, have become more prevalent.

There's no question that the conditions in today's housing market are unprecedented.

The practices that may have been effective in the past are no longer responsive

to the realities of today's housing market.

For example, appraisers generally are only required to inspect the Exterior of a

property that is being used as a comparable. But, too often, properties that have

been subject to foreclosure or distress sales have issues related to deferred maintenance

or internal damage that an external inspection cannot detect.

The NAHB believes that it's time for appraisers to have regulatory guidelines that

acknowledge such realities. In neighborhoods where the comps include a large number

of short sales or foreclosures, appraisers should have the option of expanding the

geographic area or extending the time frame for eligible sales to get a more representative

picture of the value of homes sold in the area.

The NAHB has been working on this issue for some time, and we have reached out to

the Appraisal Institute, which held an informational session at the fall board of

directors meeting last year to help builders better understand the appraisal process.

We continue to work with the Institute and other housing industry groups to address

this important issue. We have also made our position clear to the regulators who

set the standards for home sales.

What the market needs most is clear, concise regulatory guidance from Fannie and

Freddie and the housing and financial regulators that will allow appraisers to develop

realistic valuations based on sales that are truly comparable.

The bottom line is that you just cannot compare a well-constructed new home with

a foreclosed home that has been vacant for months. They simply are not "comparable,"

and the standards need to be adjusted to reflect that reality.